AGENDA

COUNCIL MEETING

Tuesday, 1 July 2025

at

9:00 AM - Budget

Council Chambers, Level 8

1 Nicholas Street, Ipswich

SONIA COOPER

Chief Executive Officer

The purpose of the meeting is to consider:

1. Adoption

of Infrastructure Levy Policy

2. Adoption

of the Annual Plan 2025-2026 (excluding Budget) - report to be provided prior

to the meeting

3. Adoption

of the 2025-2026 Budget and Associated Matters - report to be provided prior to

the meeting

4. Overall

Plan for the Rural Fire Resources Levy Special Charge

5. Rates

Timetable for 2025-2026

6. Rates

Concessions - Charitable, Non Profit/Sporting Organisations

7. Strategic

Contracting - Adoption of Annual Contracting Plan

8. Minor

amendments to Fees and Charges - Planning and Development

|

Council

Special Meeting Agenda

|

1 July

2025

|

BUSINESS

1. OPENING OF MEETING:

2. WELCOME

TO COUNTRY OR ACKNOWLEDGEMENT OF COUNTRY:

3. OPENING

PRAYER:

4. APOLOGIES

AND LEAVE OF ABSENCE:

5. DECLARATIONS

OF INTEREST IN MATTERS ON THE AGENDA:

6. OFFICERS'

REPORTS:

6.1 Adoption

of Infrastructure Levy Policy.................................. 5

6.2 Adoption

of the Annual Plan 2025-2026 (excluding Budget) - report to be provided prior

to the meeting

6.3 Adoption

of the 2025-2026 Budget and Associated Matters - report to be provided prior to

the meeting

6.4 Overall

Plan for the Rural Fire Resources Levy Special Charge............................................................................................. 13

6.5 Rates

Timetable for 2025-2026........................................... 21

6.6 Rates

Concessions - Charitable, Non Profit/Sporting Organisations....................................................................... 25

6.7 Strategic

Contracting - Adoption of Annual Contracting Plan............................................................................................. 35

6.8 Minor

amendments to Fees and Charges - Planning and Development....................................................................... 47

--ooOOoo--

|

Council

Special

Meeting Agenda

|

1 July

2025

|

Doc

ID No: A11674394

ITEM: 6.1

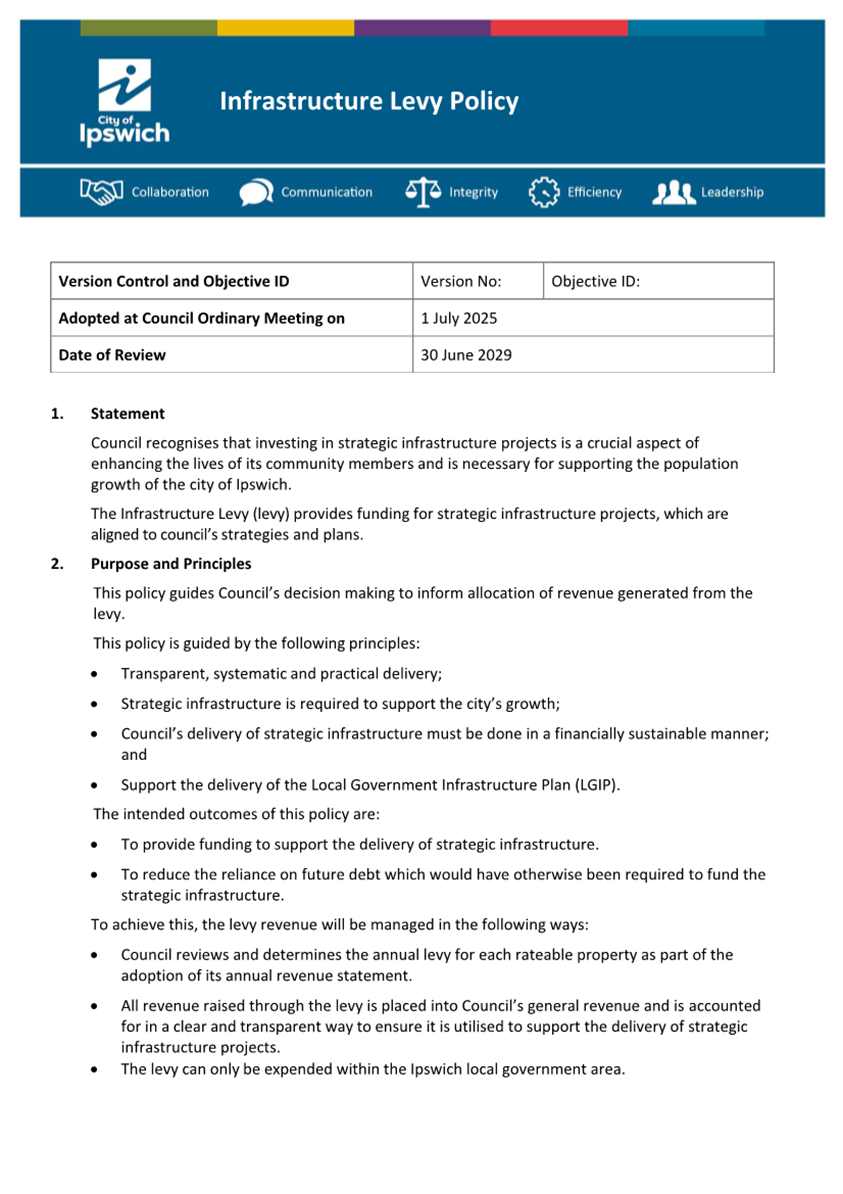

SUBJECT: Adoption of Infrastructure Levy Policy

AUTHOR: Chief Financial Officer

DATE: 18 June 2025

Executive Summary

This is a report concerning the

proposed adoption of an Infrastructure Levy Policy that supports an

Infrastructure Separate Levy (the levy), as proposed in the 2025-2025 Budget.

Recommendation/s

That Council adopt the

Infrastructure Levy Policy, as contained in Attachment 1.

RELATED PARTIES

This report deals with the

adoption of a levy policy and does not specifically reference any third party.

No conflicts of interest have been declared as of the date of this report.

ifuture Theme

Vibrant and Growing

Purpose of Report/Background

Adequate investment in strategic

infrastructure is essential to support a strong local economy and enhance the

lives of community members.

Strategic infrastructure

encompasses infrastructure outlined in the Local Government Infrastructure Plan

(LGIP) and other works significant to support the city of Ipswich’s

growth.

Councils’ assessments of the

long-term infrastructure needs of the Ipswich local government area have

identified a substantial shortfall in the funding available to progress key

development projects.

This forecast revenue gap is

illustrated by the 2024 LGIP, which outlines the key trunk projects required to

support Ipswich’s growing community over a 25 year planning horizon,

identified a sustainability ratio (the portion of required expenditure expected

to be met by forecast revenue) of less than 40% (based on the 10 year planning

horizon).

Revenue available for strategic

infrastructure projects is typically sourced from a combination of developer

contributions, grants and borrowings. These funding sources have limitations

which prevent Council from being able to adequately and expediently develop key

assets. For example, developer contributions are subject to Maximum Allowable

Charges set by the State, which is often insufficient to fund local trunk

infrastructure developments. Likewise, grants are contingent on the willingness

of external parties to progress a project, and often require co-contributions

from Council.

In order to ensure that Council

can sustainably fund key infrastructure projects, it is proposed in the

2025-2026 Budget, that provision be made to levy a separate rate for funding

strategic infrastructure on all rateable land from 1 July 2025. This proposed

policy, at Attachment 1, provides the principles behind, and basis on which the

levy willed be applied as funding for strategic projects.

Local governments are permitted to

levy separate rates and charges on rateable land, under the Local Government

Act 2009.

The levy may be expended only

within the Ipswich local government area, on strategic infrastructure projects.

The revenue raised under this levy, and its contribution to strategic projects,

will be subject to clear and transparent reporting.

Legal IMPLICATIONS

This report and its recommendations are consistent with the

following legislative provisions:

• Local

Government Act 2009

• Local

Government Regulation 2012

policy implications

The proposed new policy is consistent with, and

complimentary to Council’s existing suite of policies, specifically in

relation to financial management and infrastructure development.

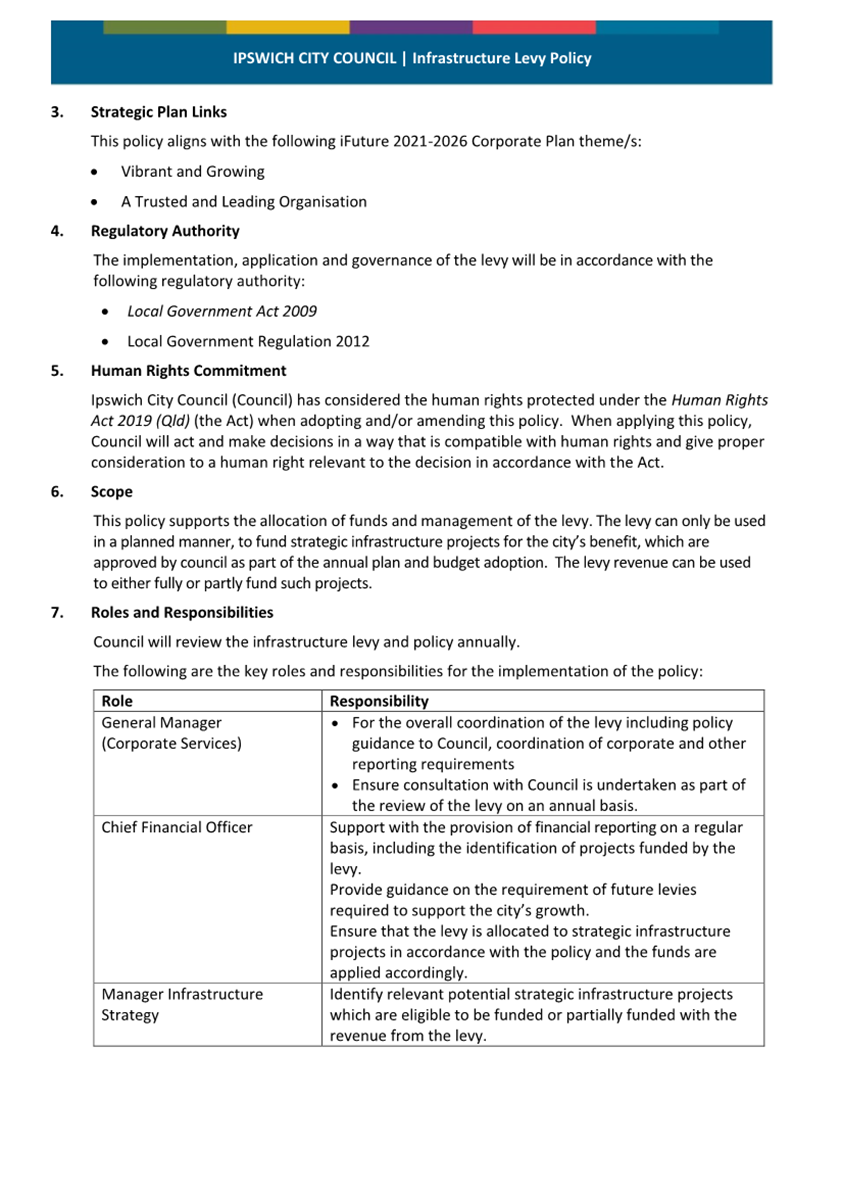

RISK MANAGEMENT IMPLICATIONS

The intent of this policy is to

permit a new mechanism for revenue generation to assist in mitigating the risks

of potential underdevelopment of strategic infrastructure in the local

government area, and/or unsustainable reliance on external debt. The

policy encompasses governance requirements to reduce financial risk.

Financial/RESOURCE IMPLICATIONS

The intent of the proposed policy

is to provide funding to support the development of key strategic

infrastructure for the benefit of the Ipswich community in a financially

sustainable manner. The annual value of funds raised by the levy will be

determined as part of the annual budget each year, and will be subject to a

specific budget resolution.

For the 2025-2026 financial year,

the levy is proposed to raise approximately $5.4 million, with the majority of

rateable land paying $55 per annum.

COMMUNITY and OTHER CONSULTATION

The Infrastructure Levy Policy has

been developed in conjunction with the 2025-2026 Budget. The Mayor and all

Councillors have been included in its development as well as the Executive

Leadership Team and senior officers across Council.

Conclusion

The adoption of this new Infrastructure Levy

Policy is proposed to provide a basis against which a separate levy may be

applied within the 2025-2026 Budget to assist in funding strategic

infrastructure within the Ipswich LGA.HUMAN RIGHTS IMPLICATIONS

|

HUMAN RIGHTS IMPACTS

|

|

OTHER DECISION

|

|

|

A11694482

|

|

(a) What

is the Act/Decision being made?

|

The Recommendation proposes that Council adopt an

Infrastructure Levy Policy. The Policy will provide a basis against which an

infrastructure rate may be applied to ratable properties.

|

|

(b) What

human rights are affected?

|

The adoption of this policy is concerned with the related

governance and application of the funds raised by the levy and does not

impact human rights. The implementation of the separate levy will be the

subject of separate report and its associated human rights assessment.

|

|

(c) How

are the human rights limited?

|

Not applicable

|

|

(d) Is

there a good reason for limiting the relevant rights? Is the limitation fair

and reasonable?

|

Not applicable

|

|

(e) Conclusion

|

The decision is consistent with human rights.

|

Attachments and Confidential Background Papers

|

1.

|

Infrastructure Levy Policy ⇩

|

Christina Binoya

Chief Financial

Officer

I concur with the recommendations contained in this

report.

Matt Smith

General Manager

(Corporate Services)

“Together,

we proudly enhance the quality of life for our community”

|

Council

Meeting

Agenda

|

1 July

2025

|

Item 6.1 / Attachment 1.

|

Council

Special

Meeting Agenda

|

1 July

2025

|

Doc ID No: A11538522

ITEM: 6.4

SUBJECT: Overall Plan for the Rural Fire Resources Levy

Special Charge

AUTHOR: Treasury Accounting Manager

DATE: 9 June 2025

Executive Summary

This

is a report concerning the adoption of an Overall Plan for the Rural Fire

Resources Levy Special Charge (the Overall Plan). The Overall Plan is

made in accordance with section 94 of the Local Government Regulation 2012

for the special benefited area adopted by Council in the 2025-2026 Budget.

Recommendation/s

That in accordance with

section 94 of the Local Government Regulation 2012, Ipswich City Council

adopt the Overall Plan, as detailed in this report, for the Rural Fire

Resources Levy Special Charge.

RELATED PARTIES

The

related parties associated with this report include:

· Rural Fire Service

· (Ipswich area) Rural Fire Brigades

· Local Area Finance Committee

· Queensland Fire Department (QFD) formerly known as

Queensland Fire and Emergency Services

ifuture Theme

A Trusted and Leading Organisation

Purpose of Report/Background

Section 94 of

the Local Government Regulation 2012 requires Council to make an overall

plan for the implementation of a special charge. The overall plan must be

adopted by resolution of Council either before or at the same time Council

resolves to levy the special rate or charge. However, the Budget

resolution making a special rate or charge must make mention of the overall

plan.

An overall plan must include the

following:

(i) describe

the service, facility or activity;

(ii) identify

the rateable land to which the special rates or charges apply;

(iii) state the

estimated cost of carrying out the overall plan; and

(iv) state the

estimated time for carrying out the overall plan.

RURAL FIRE RESOURCES LEVY SPECIAL CHARGE

OVERALL PLAN

Service, Facility or

Activity

The specially benefited area will

receive the benefit of activities and improvements funded by the Rural Fire

Brigades in the Ipswich City Council local government area, including:

(i) the

purchase of equipment not usually supplied by the Queensland Government;

(ii) maintenance

of equipment;

(iii) additional

training;

(iv) funding of

administration and day-to-day operating expenses;

(v) promotion

of the Rural Fire Services in the community and the attractive opportunity to

participate as a volunteer;

(vi) grading of

fire tracks to ensure adequate access for firefighting equipment; and

(vii) capital

improvements to rural fire brigade depots.

Identification

of the rateable land to which the Special Rates or Charges apply

In accordance with section 94 of

the Local Government Regulation 2012, Council is of the opinion that

each parcel of rateable land within the Ipswich local government area that is

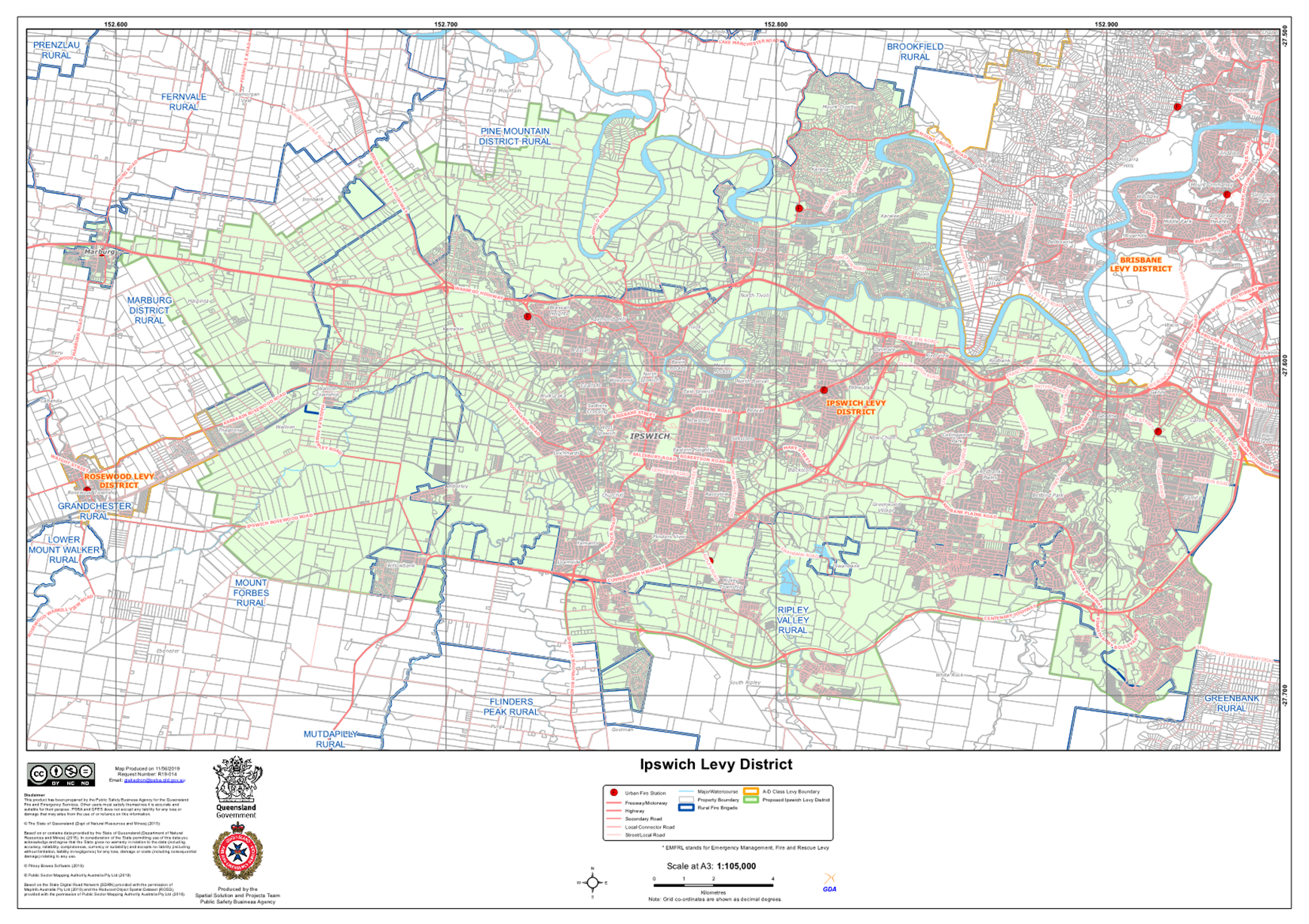

not within the boundaries of the Rosewood Levy District and Ipswich Levy

District (the Urban Fire Boundaries), as defined by the QFD and detailed in

Attachment 1, will receive a special benefit from the services, facilities and

activities funded by the Rural Fire Resources Levy Special Charge.

Estimated cost of carrying

out the Overall Plan

The total cost of carrying out the

Overall plan is estimated to be $408,000. This includes both operating

and capital expenditure components.

Estimated time for carrying

out the Overall Plan

The estimated time for carrying

out this Overall Plan is one year, being

1 July 2025 – 30 June 2026 inclusive.

Other information relevant

to the Overall Plan

On the basis that this Overall

Plan is for a period of not more than 1 year, an annual implementation plan, as

required under section 94(7) of the Local Government Regulation 2012,

is not considered necessary and has not been prepared.

Table 1 details the number of

properties that have been subject to the Rural Fire Resources Levy Special

Charge in recent years.

Table 1

|

Year

|

Properties

|

|

2024

|

3170

|

|

2025

|

3279

|

|

2026 (estimated)

|

3393

|

Table 2 details the collections

and disbursements related to the special charge for 2024‑2025. It

also includes the estimated revenue for 2025-2026 from the special charge if

adopted at $39 per annum for each parcel of rateable land as well as the

estimated disbursements.

Table 2

|

2024-2025

|

|

Unspent separate charges

carried forward from 2023-2024

|

$75,747

|

|

add special charges levied

from the 2024-2025 Overall Plan

|

$127,881

|

|

less disbursements under the

2024-2025 Overall Plan

|

$395,000

|

|

add funding received from

separate charges levied

|

$286,613

|

|

Unspent separate charges to be

carried forward

|

$95,241

|

|

2025-2026

|

|

Unspent separate charges

carried forward from 2024‑2025

|

$95,241

|

|

add special charges estimated

from the 2025-2026 Overall Plan

|

$129,988

|

|

less disbursements estimated

under the 2025-2026 Overall Plan

|

$408,000

|

|

Estimated deficit to be funded

from separate charges

|

$182,771

|

The estimated deficit for

2025-2026 is proposed to be funded by Council through the continuation of the

Rural Fire Resources Levy Separate Charge at $3 per annum levied on all

rateable land within the local government area.

To remove any

doubt, under this Overall Plan, any special charges levied will be disbursed to

the Rural Fire Brigades before any

separate charges levied. On the basis that the estimated disbursements

will exceed the estimated special charges, no surplus funds from special

charges are estimated.

Legal IMPLICATIONS

This report and its

recommendations are consistent with the following legislative provisions:

Local Government Act 2009

Local Government Regulation 2012

Fire and Emergency Services Act 1990

policy implications

There are no policy matters relevant to this report.

RISK MANAGEMENT IMPLICATIONS

The rateable land located within

the benefited area continues to benefit from the services, facilities and

activities provided by the Ipswich area Rural Fire Brigades. The

continuation of the special charge in the 2025-2026 financial year is considered

appropriate.

The growth in rateable land within

the benefited area needs to be monitored on a regular basis and Council liaise

with QFD regarding future revisions to the boundaries of the Rosewood Levy

District and Ipswich Levy District, noting that these boundaries were last

reviewed by QFD in 2019.

The continuation of any separate

charge, levied on all rateable land within the local government area, will be

subject to an annual review by Council. Any separate charge levied on all

rateable land within the local government area for the purposes of providing

funding for the services, activities and facilities under this Overall Plan, it

is not subject to this Overall Plan.

Financial/RESOURCE IMPLICATIONS

Disbursements under this Overall

Plan are estimated to be $408,000. The Rural Fire Resources Levy Special Charge

does not fully fund the estimated disbursements to the Ipswich area Rural Fire

Brigades for their services, activities and facilities and is intended to be

supplemented with funds raised by the Rural Fire Resources Levy Separate

Charge.

Any surplus funds from the Rural Fire

Resources Levy Separate Charge, will be carried forward and applied as an

available funding source for similar services, facilities or activities

provided the Rural Fire Brigades, in future budget period.

The Rural Fire Resources Levy

Special Charge and the Rural Fire Resources Levy Separate Charge are included

with Council’s proposed budget for 2025‑2026.

COMMUNITY and OTHER CONSULTATION

The financial needs of the Ipswich

area Rural Fire Brigades have been communicated to Council for

consideration. The continuation of the special charge is consistent with

previous years.

While no specific consultation has

occurred in relation to the special charge, Council has a broad understanding

of community expectations in providing support for the local area Rural Fire

Brigades. Consultation with the property owners within the benefited

area, the Ipswich area Rural Fire Brigades as well as all other landowners in

the local government area, remains an ongoing opportunity for Council to

understand community expectations in regard to the services, facilities and

activities provided by the Ipswich area Rural Fire Brigades and funded, in

part, by this special charge.

Conclusion

The rateable land within the

benefited area, being rateable land outside the Urban Fire Boundaries, continue

to specially benefit from the services, facilities and activities funded by the

Rural Fire Resources Levy Special Charge. As such, continuation of the special

charge is appropriate.

HUMAN RIGHTS IMPLICATIONS

|

HUMAN RIGHTS IMPACTS

|

|

OTHER DECISION

|

|

|

A11675936

|

|

(a) What

is the Act/Decision being made?

|

The Recommendation proposes adoption of an Overall Plan

for the Rural Fire Resources Levy Special Charge for 2025-2026.

|

|

(b) What

human rights are affected?

|

No human rights are affected by this decision. The

charges are reflective of costs and applied in an objective manner to the

properties which benefit from the services provided.

|

|

(c) How

are the human rights limited?

|

Not applicable

|

|

(d) Is

there a good reason for limiting the relevant rights? Is the limitation fair

and reasonable?

|

Not applicable

|

|

(e) Conclusion

|

The decision is consistent with human rights.

|

Attachments and Confidential Background Papers

|

1.

|

QFES District Boundaries ⇩

|

Paul Mollenhauer

Treasury

Accounting Manager

I concur with the recommendations contained in this

report.

Christina Binoya

Chief Financial

Officer

I concur with the recommendations contained in this

report.

Matt Smith

General Manager

(Corporate Services)

“Together,

we proudly enhance the quality of life for our community”

|

Council

Meeting

Agenda

|

1 July

2025

|

Item 6.4 / Attachment 1.

|

Council

Special

Meeting Agenda

|

1 July

2025

|

Doc

ID No: A11537197

ITEM: 6.5

SUBJECT: Rates Timetable for 2025-2026

AUTHOR: Treasury Accounting Manager

DATE: 9 June 2025

Executive Summary

This is a report concerning the

issuance date, as well as the discount and due date, for payment for the

quarterly rates for the 2025-2026 year.

Recommendation/s

That in accordance with

section 118 of the Local Government Regulation 2012, Ipswich City

Council decide the dates by which rates and charges for 2025-2026 must be paid,

as detailed in Table 1:

Table 1

|

Period

|

Due Date for Payment

|

|

July to September 2025

|

Thursday 21 August 2025

|

|

October to December 2025

|

Thursday 20 November 2025

|

|

January to March 2026

|

Thursday 19 February 2026

|

|

April to June 2026

|

Thursday 21 May 2026

|

RELATED PARTIES

There are no related party matters

associated with this report.

ifuture Theme

A Trusted and Leading Organisation

Purpose of Report/Background

Council adopts a timetable for the

issue of rate notices as well as the discount and due date for payment for each

quarter of the financial year. Where practical, a 13 week cycle between

due dates in successive quarters is maintained.

Due to the time required to update

the system with the new parameters, the rates generation and consequently the

issue date, for the July to September 2025 has been extended a week.

Consequently, the period between the last issue date and July to September 2025

will be 14 weeks.

Each quarterly rates notice needs

to be issued at least 30 days before the due date.

The following is the proposed

timetable for the 2025-2026 financial year. The proposed timetable takes

into account sufficient time to print and issue rate notices as well as

standard postage service times.

|

Period

|

Issue Date

|

Discount and Due Date for

payment

|

Period for last Due Date

|

|

July to September 2025

|

Friday

18 July 2025

|

Thursday

21 August 2025

|

14 Weeks

|

|

October to December 2025

|

Friday

17 October 2025

|

Thursday

20 November 2025

|

13 Weeks

|

|

January to March 2026

|

Friday

16 January 2026

|

Thursday

19 February 2026

|

13 Weeks

|

|

April to June 2026

|

Friday

17 April 2026

|

Thursday

21 May 2026

|

13 Weeks

|

The issue date of the next

quarter’s rates notice is displayed on each rates notice.

Legal IMPLICATIONS

This report and its recommendations are consistent with the

following legislative provisions:

Local Government Regulation 2012

policy implications

There are no policy implications related to this report.

RISK MANAGEMENT IMPLICATIONS

There are no significant risk

management implications associated with this report.

Financial/RESOURCE IMPLICATIONS

As this report relates only to the

timing of rates notices rather than the setting of rates charges, there are no

specific financial or resource implications of not associated with this

report. Councils’ proposed 2025-2026 budget and financial modelling

takes into account the proposed quarterly rating schedule.

COMMUNITY and OTHER CONSULTATION

No community consultation has been

undertaken in relation to this report. No material changes have been

proposed to current rating practise.

Conclusion

The proposed issue date, discount

and due date for payment for the quarterly rates notices continue to be timed

around a 13-week cycle, where possible.

HUMAN RIGHTS IMPLICATIONS

|

HUMAN RIGHTS IMPACTS

|

|

OTHER DECISION

|

|

|

A11704892

|

|

(a) What

is the Act/Decision being made?

|

The Recommendation requests that Council decide the dates

by which rates and charges for the 2025-2026 must be paid.

|

|

(b) What

human rights are affected?

|

No human rights are affected, as this decision relates

only to the timing of the issuance and payment of rates notices, and the

timing is applicable to all ratepayers equally.

|

|

(c) How

are the human rights limited?

|

Not Applicable

|

|

(d) Is

there a good reason for limiting the relevant rights? Is the limitation fair

and reasonable?

|

Not Applicable

|

|

(e) Conclusion

|

The decision is consistent with human rights.

|

Paul Mollenhauer

Treasury Accounting

Manager

I concur with the recommendations contained in this

report.

Christina Binoya

Chief Financial

Officer

I concur with the recommendations contained in this

report.

Matt Smith

General Manager

(Corporate Services)

“Together,

we proudly enhance the quality of life for our community”

|

Council

Special

Meeting Agenda

|

1 July

2025

|

Doc

ID No: A11546756

ITEM: 6.6

SUBJECT: Rates Concessions - Charitable, Non

Profit/Sporting Organisations

AUTHOR: Treasury Accounting Manager

DATE: 9 June 2025

Executive Summary

This is a report concerning the

annual review and approval of rates concessions to eligible Charitable and

Non-Profit/Sporting Organisations in accordance with Ipswich City

Council’s (Council) Rates Concession Policy.

Recommendation/s

That having satisfied the

criteria in s120 of the Local Government Regulation 2012, as well as the

Rates Concession Policy, the properties as detailed in Attachment 1 be granted

a 100% concession of the differential general rates for the 2025-2026 financial

year.

RELATED PARTIES

Mayor and Councillors should

consider those entities listed in the attachments to this report. No potential

conflicts of interest have been identified prior to the submission of this

report.

ifuture Theme

A Trusted and Leading Organisation

Purpose of Report/Background

The Local Government Act

2009 and Local Government Regulation 2012 describes the circumstances

where Council may approve a concession for rates and charges levied for a

particular class of properties or to owners of specific properties.

The remission of rates for

pensioners is an example of a concession available to a class of property

owners. The remission of rates for pensioners is not detailed in this

report.

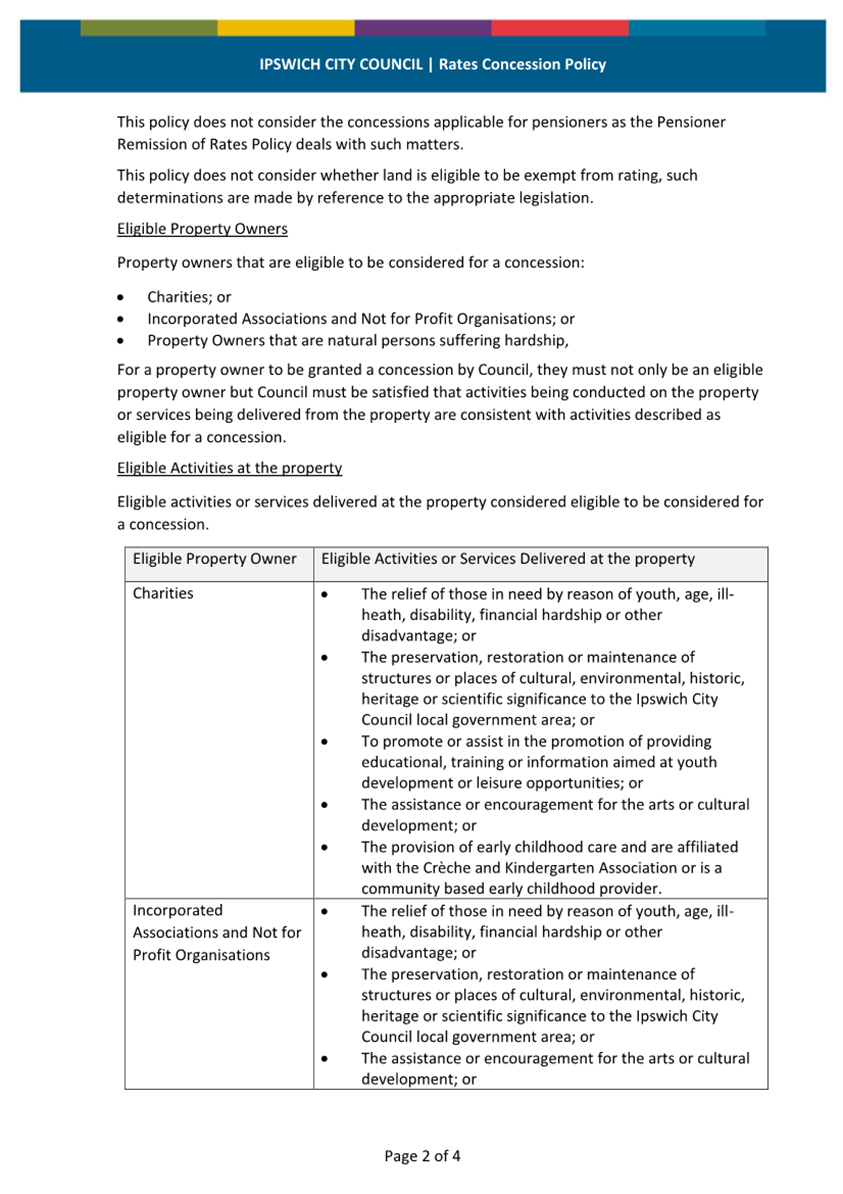

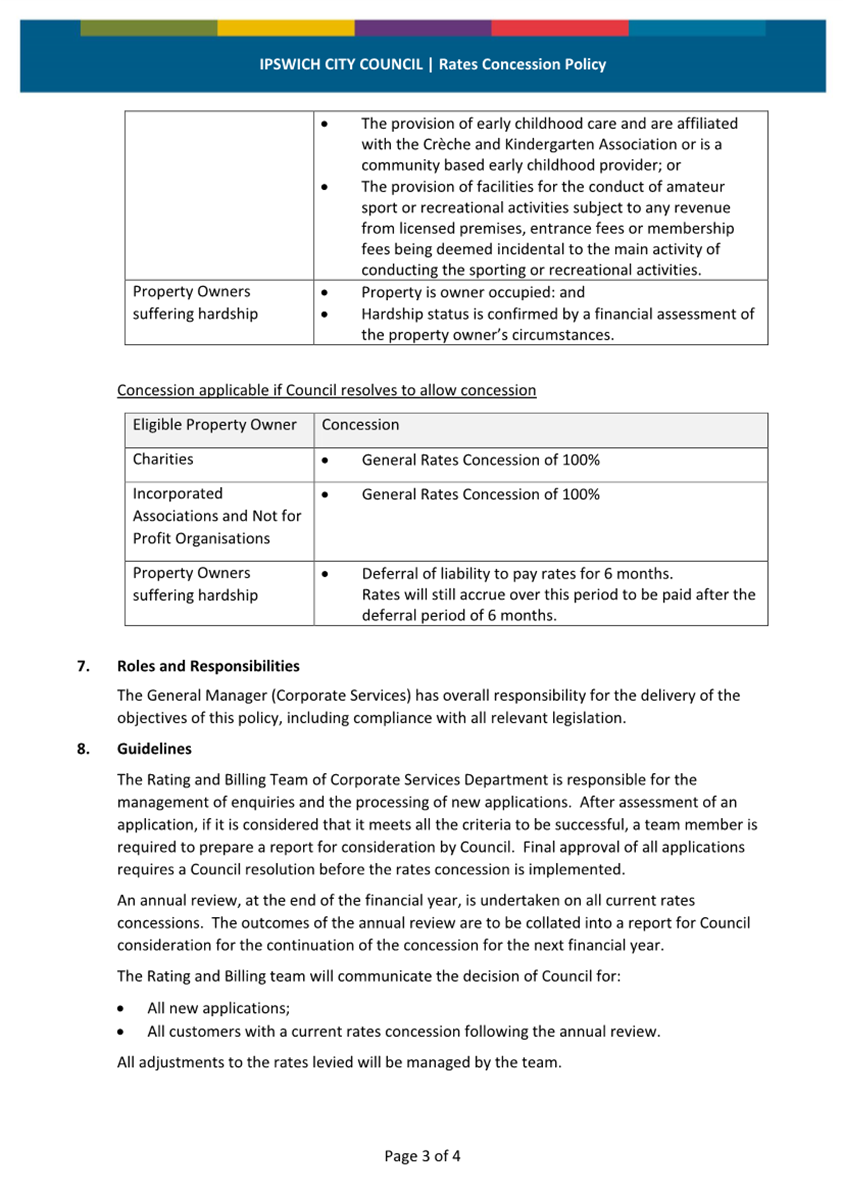

Council has adopted a Rates

Concession Policy which outlines the criteria used to determine eligibility of

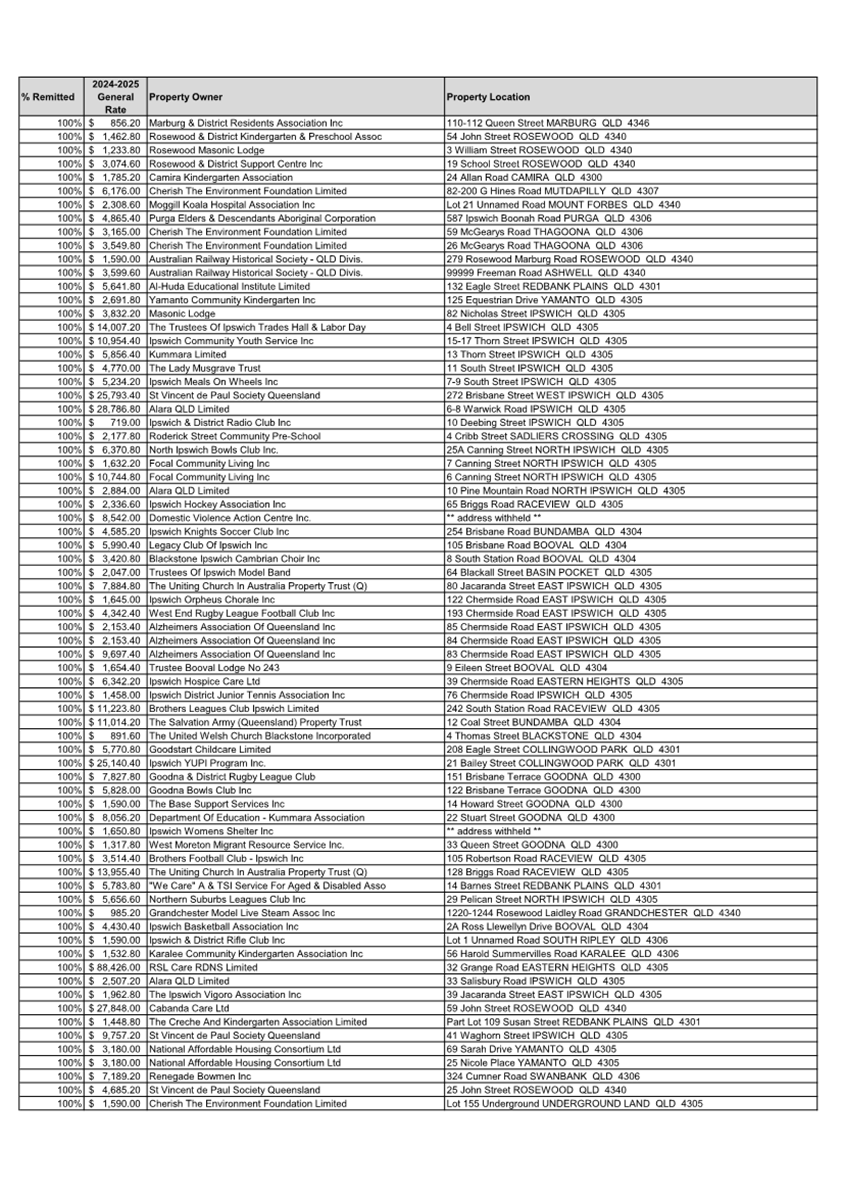

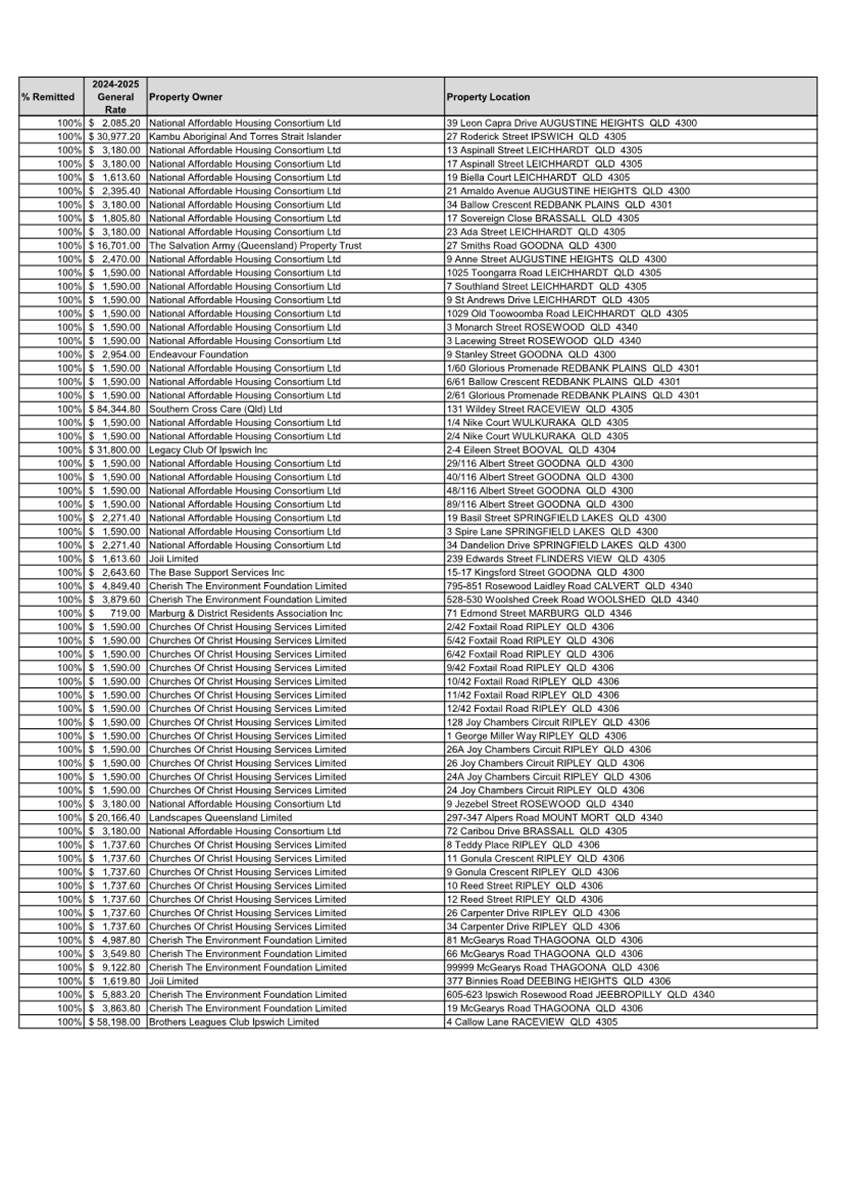

organisations and properties for a concession. Currently there are 140

properties that have been previously approved for a concession of 100% of the

differential general rates levied. These properties are described in

Attachments 1. For convenience a copy of the Rates Concession Policy is

included at Attachment 2.

In accordance with the policy, a

review of properties and organisations receiving a concession is undertaken

annually. This involves a review of the land use of the subject property, the

ownership of the land and the operations of the organisation concerned.

This review has been undertaken and no changes to the eligibility for a

concession under the policy, have been identified for the properties listed in

Attachments 1.

Council exempts properties from

being assessable from Council rates in accordance with section 93(3) of the Local

Government Act 2009 and section 73 of the Local Government Regulation

2012. Land that is exempt from rates is considered and determined in

accordance with the relevant legislation. This report does not consider

exemption from rates.

Legal IMPLICATIONS

This report and its recommendations are consistent with the

following legislative provisions:

Local Government Act 2009

Local Government Regulation 2012

policy implications

This report is consistent with the

annual review as part of the Rates Concession Policy

RISK MANAGEMENT IMPLICATIONS

There are no risk management

implications associated with this report.

Financial/RESOURCE IMPLICATIONS

The annual equivalent of general

rates concessions in 2024-2025 was approximately $880,000. The value of

concessions for 2025-2026 will be determined at the time of each quarterly

rates generation and is anticipated to be an annual equivalent of approximately

$924,000, subject to any future application by eligible property owners and the

subsequent approval of Council.

COMMUNITY and OTHER CONSULTATION

The contents of this report did

not require any community consultation. The proposed concessions are granted

consistent with adopted policy.

Conclusion

Council has adopted a Rates

Concession Policy for approving of concessions to qualifying organisations and

properties. Currently there are 140 properties that have been previously

approved for a concession of 100% of the differential general rates levied.

Following a review of the legislative and policy criteria, those properties

continue to be eligible for a concession in 2025-2026.

HUMAN RIGHTS IMPLICATIONS

|

HUMAN RIGHTS IMPACTS

|

|

OTHER DECISION

|

|

|

A11704889

|

|

(a) What

is the Act/Decision being made?

|

The recommendation requests the approval of rates

concessions to eligible Charitable and Non-Profit/Sporting Organisations in

accordance with Ipswich City Council’s (Council) Rates Concession

Policy

|

|

(b) What

human rights are affected?

|

No human rights are affected. The concessions detailed in

this report are not provided to individuals. This decision seeks to provide

financial relief from the payment of differential general rates to eligible

ratepaying organisations which are expected to provide a charitable or other

benefit to the local community through the use of that rateable

property. Eligibility is based on the attributes of the ratepayer, and

as such is not arbitrary.

|

|

(c) How

are the human rights limited?

|

Not applicable

|

|

(d) Is

there a good reason for limiting the relevant rights? Is the limitation fair

and reasonable?

|

Not applicable

|

|

(e) Conclusion

|

The decision is consistent with human rights.

|

Attachments and Confidential Background Papers

|

1.

|

List of eligible organisations for concession ⇩

|

|

2.

|

Rates Concession Policy ⇩

|

Paul Mollenhauer

Treasury

Accounting Manager

I concur with the recommendations contained in this

report.

Christina Binoya

Chief Financial

Officer

I concur with the recommendations contained in this

report.

Matt Smith

General Manager

(Corporate Services)

“Together,

we proudly enhance the quality of life for our community”

|

Council

Meeting

Agenda

|

1 July

2025

|

Item 6.6 / Attachment 1.

|

Council

Meeting

Agenda

|

1 July

2025

|

Item 6.6 / Attachment 2.

|

Council

Special

Meeting Agenda

|

1 July

2025

|

Doc

ID No: A11644527

ITEM: 6.7

SUBJECT: Strategic Contracting - Adoption of Annual

Contracting Plan

AUTHOR: Manager, Procurement

DATE: 30 May 2025

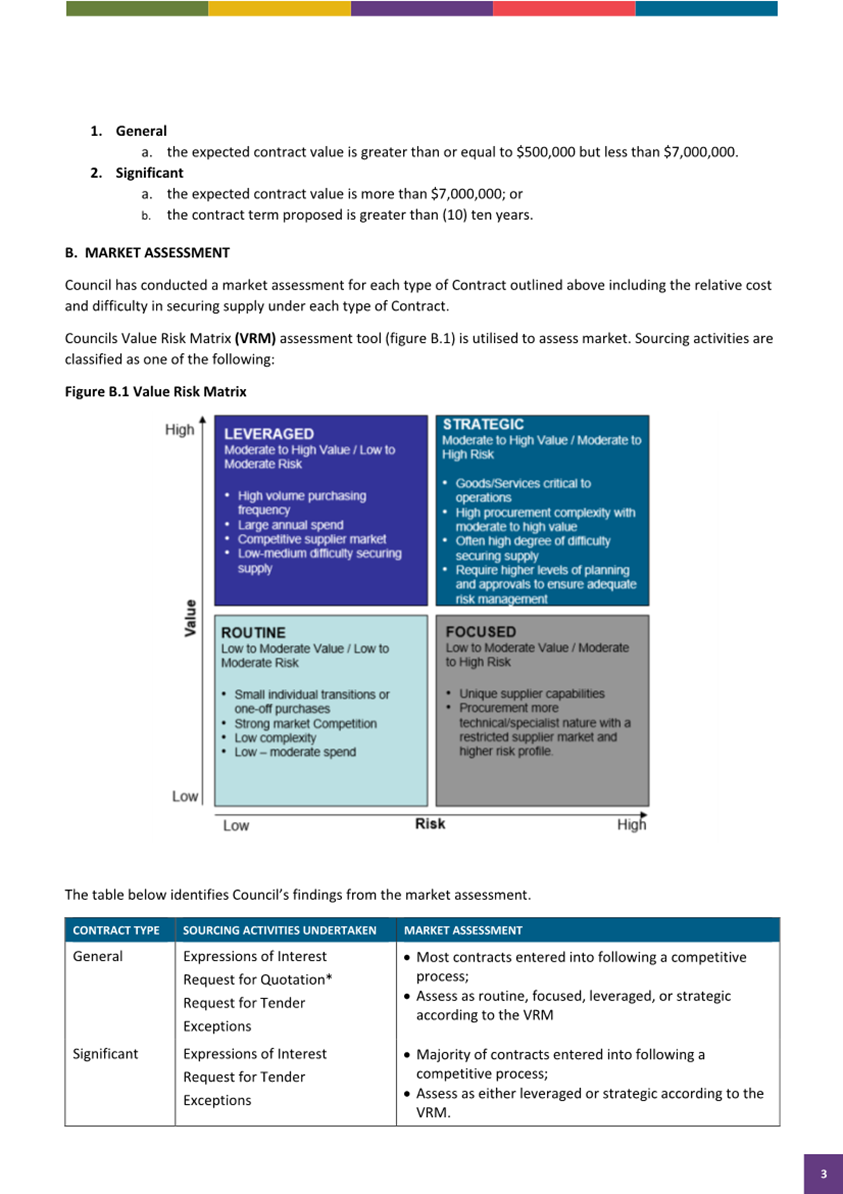

Executive Summary

This is a report concerning the

adoption of ‘Strategic Contracting Procedures’ (SCP) from

1 July 2025 for Council contracts, as per the requirements of Chapter 6, Part 2

of the Local Government Regulation 2012.

Recommendation/s

That pursuant to section

220(2) of the Local Government Regulation 2012, Council adopt the Annual

Contracting Plan (ACP) (as contained as Attachment 1 to this Report) for the

2025-2026 Financial Year.

RELATED PARTIES

There are

no declarations of conflicts of interest.

All Council Suppliers

All Council Employees

ifuture Theme

A Trusted and Leading Organisation

Purpose of Report/Background

On 30 April 2025 Council resolved

to apply Chapter 6, Part 2 ‘Strategic Contracting Procedures’ (SCP)

of the Local Government Regulation 2012 (the Regulation) to its

contracts from 1 July 2025.

On 19 June 2025 Council resolved

to adopt the Procurement Policy and the Procurement and Contracts Manual which

aligns with Council’s Strategic Contracting Procedures governance

framework and sets out Council’s procedures for carrying out all

contracts from 1 July 2025.

Pursuant with the adoption of the

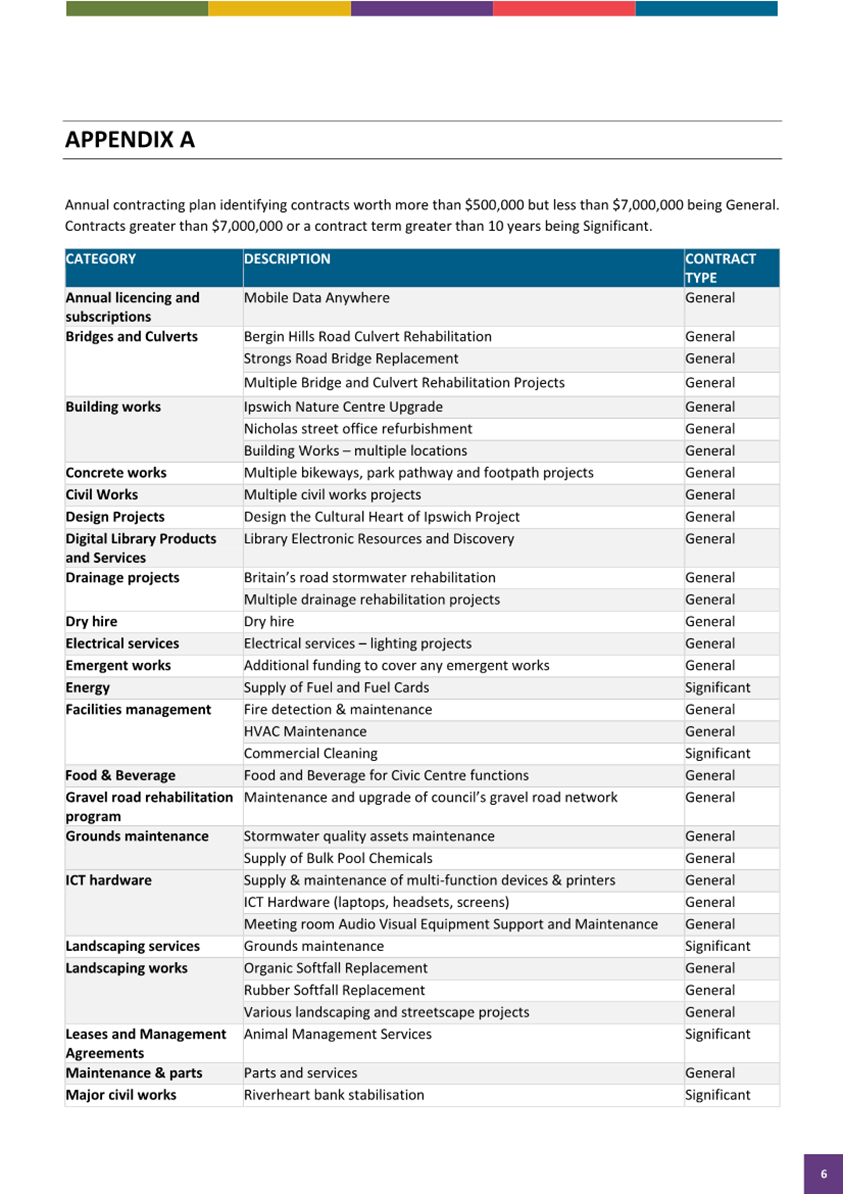

Strategic Contracting Procedures, the Council is required to adopt the ACP for

the 2025-2026 Financial year, after the adoption of the annual budget for the

Financial Year.

The ACP was submitted for noting

in report titled ‘Strategic

Contracting - Adoption of Annual Contracting Plan’ presented to

the Finance and Governance Committee meeting on 10 June. The

2025-2026 ACP is now presented for adoption by Council, as contained in

Attachment 1 to this report.

Legal IMPLICATIONS

This report and its recommendations are consistent with the

following legislative provisions:

Local Government Act 2009

Local Government Regulation 2012

policy implications

This decision is consistent with the Procurement Policy and

the Procurement and Contracts Manual which were adopted by Council on 19 June

2025.

RISK MANAGEMENT IMPLICATIONS

The SCP is an approach that

identifies potential opportunities, while managing adverse risks as per section

217(2) of the Regulation.

Financial/RESOURCE IMPLICATIONS

The delivery of the SCP is

consistent with the existing budget. The costs and benefits of applying the

Strategic Contracting Procedures were reported to Council on 18 February 2025.

The strategic approach would cost no more, and likely less than the costs

associated with maintaining the existing framework under the Default

Contracting Procedures.

COMMUNITY and OTHER CONSULTATION

Consultation has occurred with the

Executive Leadership Team, Procurement Branch, Legal and Governance and

selected stakeholders within Council.

Conclusion

The shift to SCP under Part 2,

Chapter 6 of the Regulation marks a significant milestone for Council in

strengthening its procurement capabilities and improving operational

efficiency. The Procurement Policy and the Procurement and Contracts Manual

were adopted by Council on 19 June 2025. The adoption of the ACP marks

the final step in the shift from default contracting procedures to Strategic

Contracting Procedures for Council.

HUMAN RIGHTS IMPLICATIONS

|

HUMAN RIGHTS IMPACTS

|

|

OTHER DECISION

|

|

|

|

|

(a) What

is the Act/Decision being made?

|

Council resolves to adopt the Annual Contracting Plan (as

contained as Attachment 1 to this Report) for the 2025-2026 Financial Year.

|

|

(b) What

human rights are affected?

|

No Human rights are affected by this decision

|

|

(c) How

are the human rights limited?

|

Not applicable

|

|

(d) Is

there a good reason for limiting the relevant rights? Is the limitation fair

and reasonable?

|

Not applicable

|

|

(e) Conclusion

|

The decision is consistent with human rights.

|

Attachments and Confidential Background Papers

|

1.

|

Annual Contracting Plan (FY25-26) ⇩

|

Tanya Houwen

Manager,

Procurement

I concur with the recommendations contained in this

report.

Matt Smith

General Manager (Corporate

Services)

“Together,

we proudly enhance the quality of life for our community”

|

Council

Meeting

Agenda

|

1 July

2025

|

Item 6.7 / Attachment 1.

|

Council

Special

Meeting Agenda

|

1 July

2025

|

Doc

ID No: A11674389

ITEM: 6.8

SUBJECT: Minor amendments to Fees and Charges -

Planning and Development

AUTHOR: Treasury Accounting Manager

DATE: 9 June 2025

Executive Summary

This is a report concerning the

adoption of minor amendments to the fees and charges for planning services to

apply from 1 July 2025.

Recommendation/s

That the proposed amendments

to Fees and Charges for planning services, as outlined in Attachment 1, be

adopted with an effective date of 1 July 2025.

RELATED PARTIES

This report deals with the

adoption of the pricing of fees and charges and does not specifically reference

any third party.

ifuture Theme

A Trusted and Leading Organisation

Purpose of Report/Background

Section 98 of the Local Government

Act 2009 (LGA) requires Council to maintain a publicly available register of

cost recovery fees.

As part of the annual budget

adoption process, Council undertakes a review of all fees and charges prior to

the commencement of a new financial year. Fees for the 2025-2026

financial year were subject to approval at the meetings of 27 March 2025 (for

health and regulatory services fees), and 29 May 2025 for all other fees.

A small number of further

amendments to the register are proposed to provide greater clarity as to the

application of service fees. The proposed amendments, as outlined in Attachment

1, include:

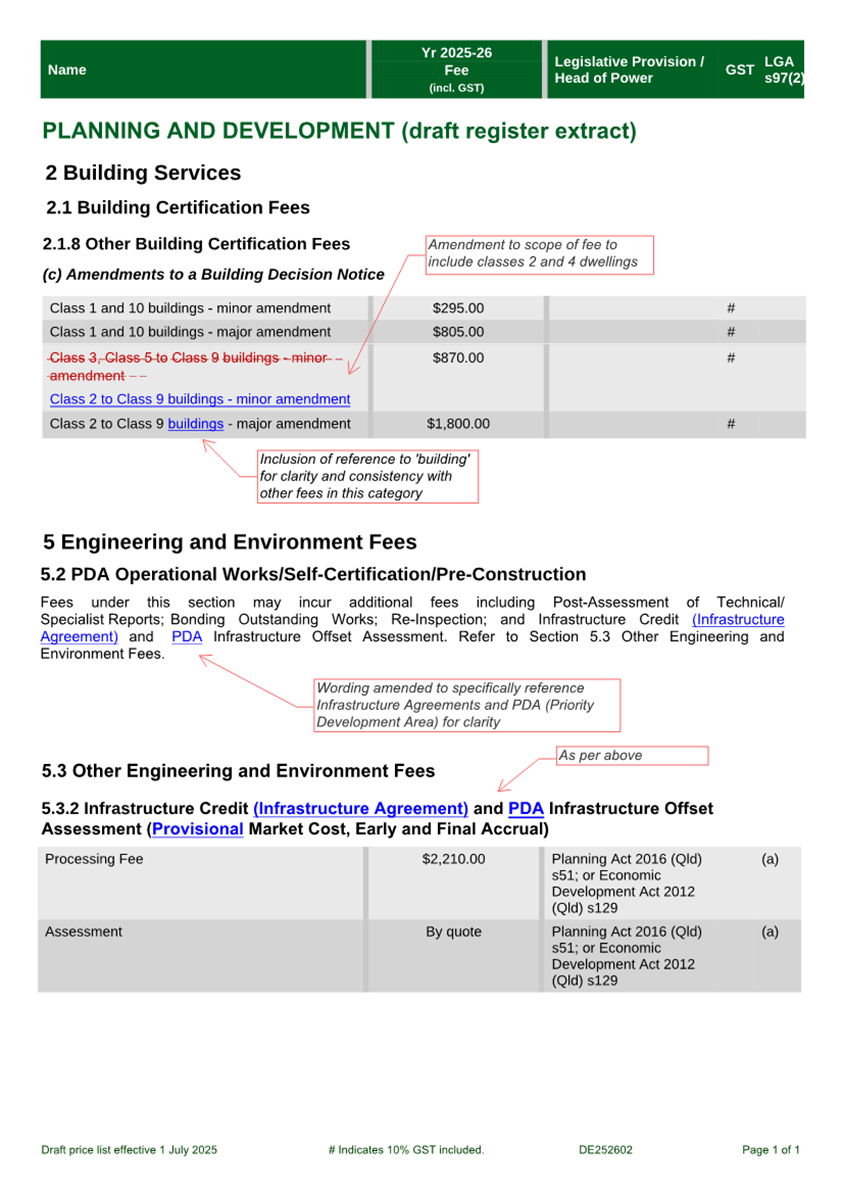

a) Increasing

the scope of fees for minor amendments to building certifications to include

class 2 and 4 dwellings, consistent with the categorisations for major

amendments, and

b) In

the Engineering and Environment Fees section, specifying that Infrastructure

Credits are applicable to Infrastructure Agreements, and Infrastructure Offsets

Assessments relate to Priority Development Areas (PDA).

No changes are proposed to the

value of the approved fees.

Legal IMPLICATIONS

This report and its recommendations are consistent with the

following legislative provisions:

Local Government Act 2009 s97 and 98

policy implications

The proposed amendments are consistent with Council’s

planning scheme and policies.

Fees and charges are established in accordance with Councils

Revenue Policy.

RISK MANAGEMENT IMPLICATIONS

The intent of the proposed

clarifications to the register of fees and charges is to mitigate any potential

risk of the planning fees being incorrectly applied.

Financial/RESOURCE IMPLICATIONS

The proposed amendments are for

clarification purposes only, and will not result in any direct financial

implications for Council or external stakeholders.

COMMUNITY and OTHER CONSULTATION

This proposal was initiated by,

and developed in consultation with the Planning and Regulatory Services

department.

Due to the administrative nature

of the proposed amendments, consultation with external parties was not

warranted.

Conclusion

It is recommended that Council

approve the proposed variations and additions to the Register of Fees and

Charges.

HUMAN RIGHTS IMPLICATIONS

|

HUMAN RIGHTS IMPACTS

|

|

OTHER DECISION

|

|

|

A11675936

|

|

(a) What

is the Act/Decision being made?

|

The Recommendation seeks Council approval for proposed

minor amendments to Fees and Charges for planning services.

|

|

(b) What

human rights are affected?

|

This decision has the potential to impact human rights in

relation to recognition and equality before the law.

|

|

(c) How

are the human rights limited?

|

The amendments to the application of planning fees may

impact some customers requiring these services as part of planning and

development activities.

|

|

(d) Is

there a good reason for limiting the relevant rights? Is the limitation fair

and reasonable?

|

The fees and charges the proposed amendments apply to do

not apply to core Council services or public goods, but rather to services

which are optional to take up and benefit an individual.Where charges are

applied, this is enabled by, and governed by legislative provisions. For

services which can be provided by a Local Government only, Council is

required to charge not more than cost recovery.

|

|

(e) Conclusion

|

The decision is consistent with human rights.

|

Attachments and Confidential Background Papers

|

1

|

Proposed Planning Fee Amendments ⇩

|

Paul Mollenhauer

Treasury

Accounting Manager

I concur with the recommendations contained in this

report.

Christina Binoya

Chief Financial

Officer

I concur with the recommendations contained in this

report.

Matt Smith

General Manager

(Corporate Services)

“Together,

we proudly enhance the quality of life for our community”

|

Council

Meeting

Agenda

|

1 July

2025

|

Item 6.8 / Attachment 1