|

Audit and Risk Management Committee Meeting Agenda |

6 November 2019 |

The Chairperson has determined this matter is of real urgency and approval has been given to refer this report to the Audit and Risk Management Committee as a late item.

ITEM: 1

SUBJECT: Asset Valuation - Land, Buildings and Infrastructure Assets

AUTHOR: Principal Financial Accountant

DATE: 30 October 2019

Executive Summary

This is a report by the Principal Financial Accountant dated the 30 October 2019 concerning the engagement of a qualified valuer to perform asset revaluation services of Council’s land, building and infrastructure assets over the next five (5) years.

Recommendation/s

That the Interim Administrator of Ipswich City Council resolves:

That Council endorse the request for quotation process for the engagement of a qualified valuer for five (5) years to perform asset revaluation services as outlined in the report by the Principal Financial Accountant dated 30 October 2019.

RELATED PARTIES

There are no related parties.

Advance Ipswich Theme

Listening, leading and financial management

Purpose of Report/Background

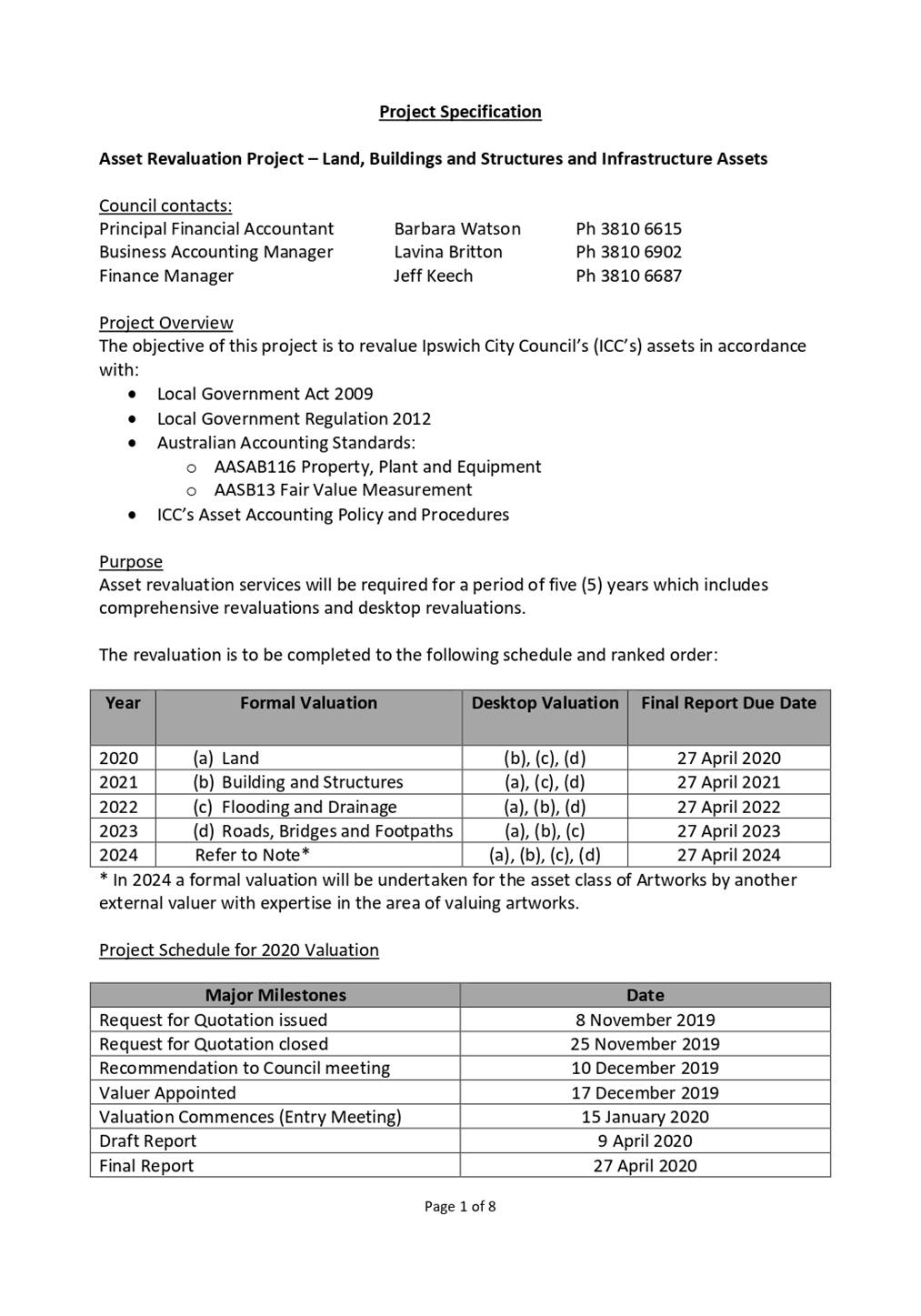

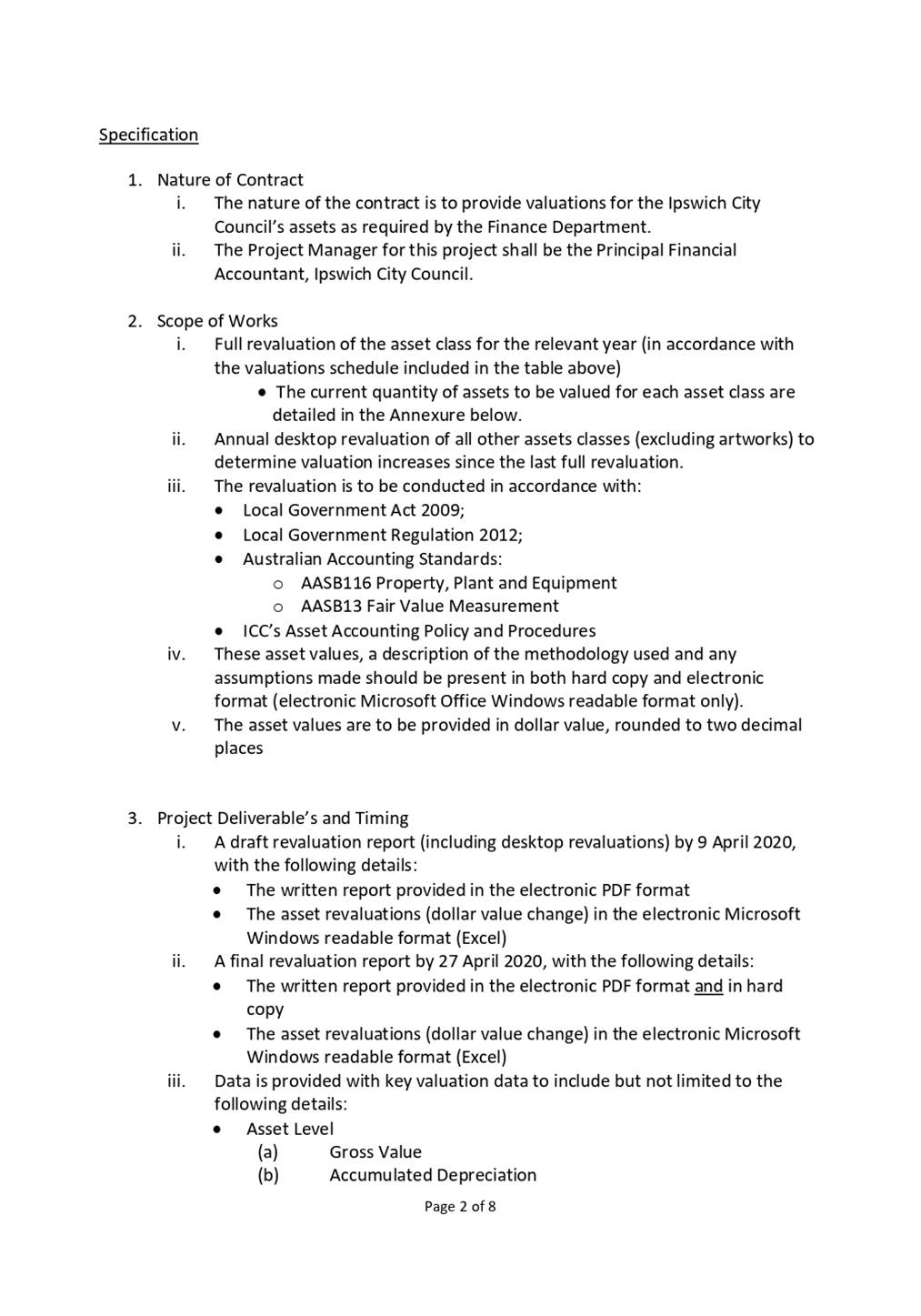

In accordance with Council’s Asset Accounting Policy and Asset Revaluation Procedure and the Australian Accounting Standards, Council is required to conduct an annual revaluation for its non-current asset classes: artworks, land, buildings and structures, drainage, and roads, bridges and footpaths. This memorandum specifically deals with asset revaluation for land, buildings and structures, drainage, and roads, bridges and footpath assets.

Council’s current revaluation procedure Asset Revaluation FCS-005 provides that Council will revalue all its non-current assets on a five year rolling basis provided that these assets do not experience significant and volatile change in fair value.

The current revaluation schedule is as follows:

|

Year |

Formal Valuation |

Desktop Valuation |

Final Report Due Date |

|

2020 |

(a) Land |

(b), (c), (d) |

27 April 2020 |

|

2021 |

(b) Building and Structures |

(a), (c), (d) |

27 April 2021 |

|

2022 |

(c) Flooding and Drainage |

(a), (b), (d) |

27 April 2022 |

|

2023 |

(d) Roads, Bridges and Footpaths |

(a), (b), (c) |

27 April 2023 |

|

2024 |

Refer to Note* |

(a), (b), (c), (d) |

27 April 2024 |

* In 2024 a formal valuation will be undertaken for the asset class of Artworks by another external valuer with expertise in the area of valuing artworks.

Before commencing the annual revaluation, Council will make an annual assessment to determine whether there have been significant market movements and/or changes to local conditions to necessitate the revaluation schedule to be brought forward or maintained.

An assessment was completed in October 2019 by Finance in collaboration with Council’s Senior Planning Officer (Asset Management) in Infrastructure and Environment Department (IE) with the recommendation that this schedule be maintained for 2019-2020 asset revaluation exercise.

Council’s five (5) year contract with Cardno (QLD) Pty Ltd for supply of asset valuation services recently expired. In accordance with Council’s Procurement Policy and “sound contracting principles” in section 104 of the Local Government Act 2009, Council will request quotations for asset valuation services for the next five (5) years the Local Buy panel. Through consultation with Council’s Procurement Team and Asset Management Team it is recommended that the following three (3) suppliers from Local Buy be invited to quote.

· Cardno (QLD Pty) Ltd

· GHD Pty Ltd

· JLL Public Sector Valuations Pty Ltd (Formerly Australian Valuation Solutions Pty Ltd)

Council’s current policy does not require a rotation of valuers however this can be discussed further with the Committee to determine if consideration should be given to an amendment to the policy in the future.

In consultation with Council’s Procurement Team and Asset Management Team, the below schedule outlines key milestones for the engagement of a valuer for the next five (5) years and valuation of Council’s assets for 2019-2020.

|

Key Milestones |

Date |

|

Request for Quotation issued |

8 November 2019 |

|

Request for Quotation closed |

25 November 2019 |

|

Recommendation to Council meeting |

10 December 2019 |

|

Valuer Appointed |

17 December 2019 |

|

Valuation Commences (Entry Meeting) |

15 January 2020 |

|

Draft Report |

9 April 2020 |

|

Final Report |

27 April 2020 |

The evaluation team will be facilitated by the Procurement Team and include representatives from both Council’s Finance and Asset Management teams, with a final recommendation being provided through the General Management Corporate Services to Council for approval as the term of the contract is for 5 years.

Legal/Policy Basis

This report and its recommendations are consistent with the following legislative provisions:

Local Government Act 2009

Local Government Regulation 2012

Australian Accounting Standards

RISK MANAGEMENT IMPLICATIONS

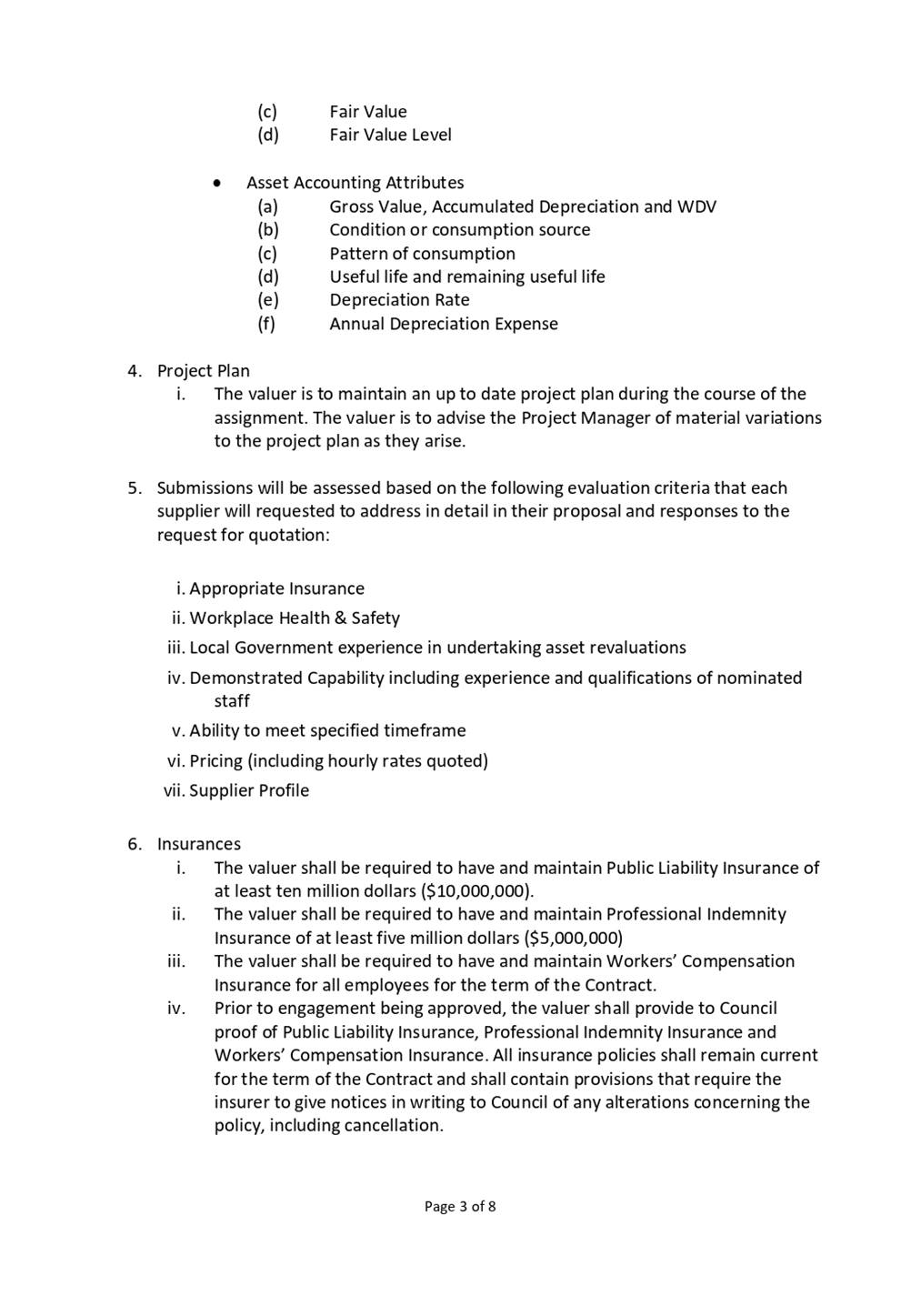

The valuation of assets in accordance with the Accounting Standards, including AASB 116 Property, Plant and Equipment & AAS13 Fair Value, is a significant risk as part of the preparation of the Annual Financial Statements and compliance with Council’s Asset Accounting policy. Council processes, the management and involvement of appropriate qualified and skilled Council staff and support from an experienced qualified valuation expert, are critical to mitigating this risk.

Risks associated with not obtaining quotes from at least three (3) suppliers for asset valuation services for the next five (5) years would result in not adhering to Council’s Procurement Policy and sound contracting principles (eg. value for money, open and effective competition) as per section 104 of the Local Government Act 2009.

As part of Transformational Project 4 (Asset Management), Council is continuing to update its asset management systems and databases which is likely to impact on the information detail within the Physical Asset Registers. Council will need to ensure that scoping with the preferred valuer communicates that there will likely be changes to the format of data presented during the 5 years to minimise any changes to pricing. Council will also request hourly rate pricing as part of quotations to assist in mitigating this. The continued close working of the asset management team and asset accounting team is also extremely important in ensure accurate and timely revaluations.

Financial/RESOURCE IMPLICATIONS

The anticipated budget for asset valuation services for the next five (5) years which is included in our financial forecasts, is approximately $250,000 - $300,000 excluding GST, subject to the quotation process.

COMMUNITY and OTHER CONSULTATION

The asset management team have been consulted with and are part of the team reviewing the specifications and evaluation of quotations received. The procurement process is being led by Council’s procurement team.

Conclusion

Following the expiration of Council’s contract with Cardno (QLD) Pty Ltd for asset valuation services Council will request quotations through Local Buy to request quotes from suitably qualified valuers for asset valuation services with the term of engagement over the next five (5) years.

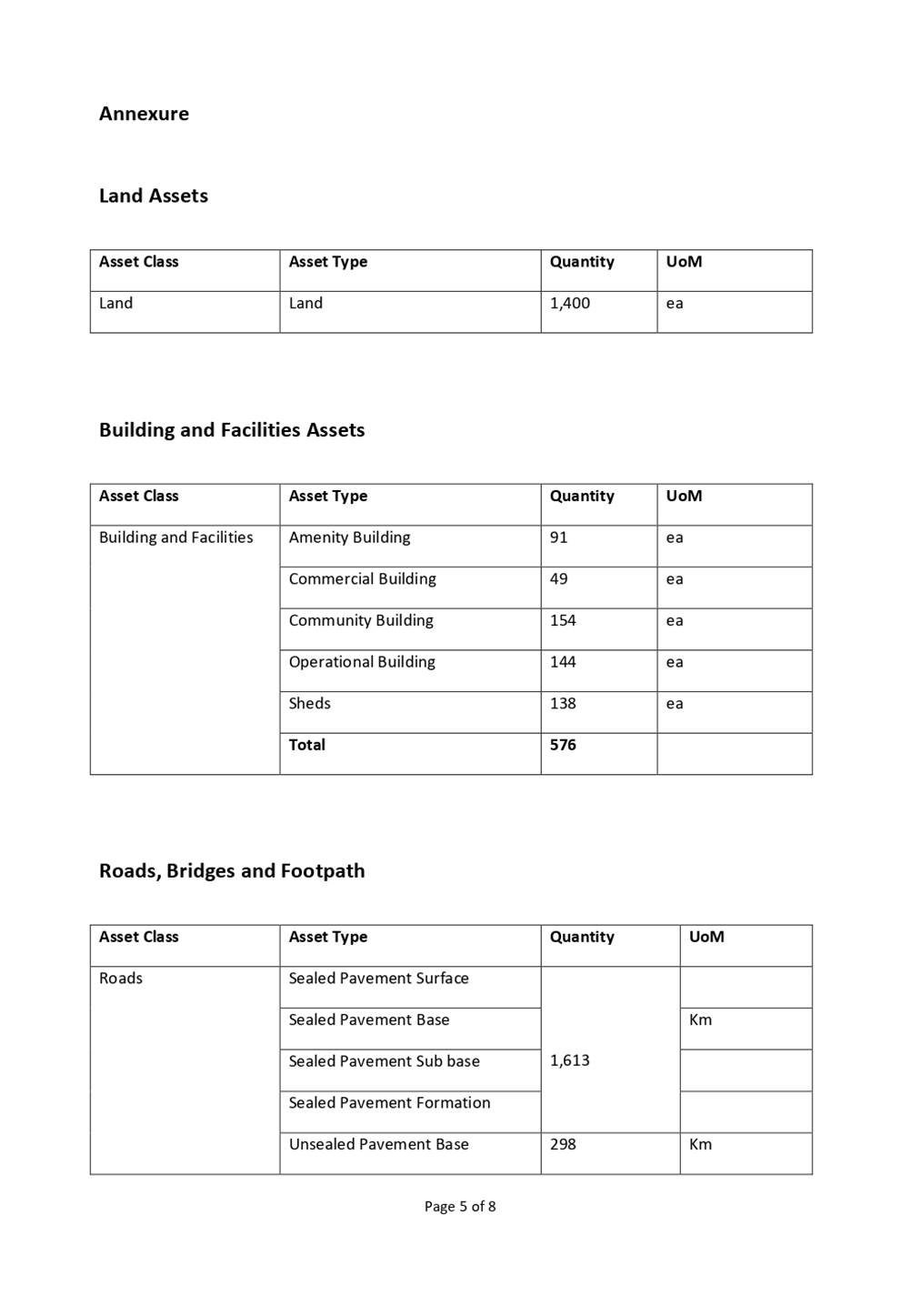

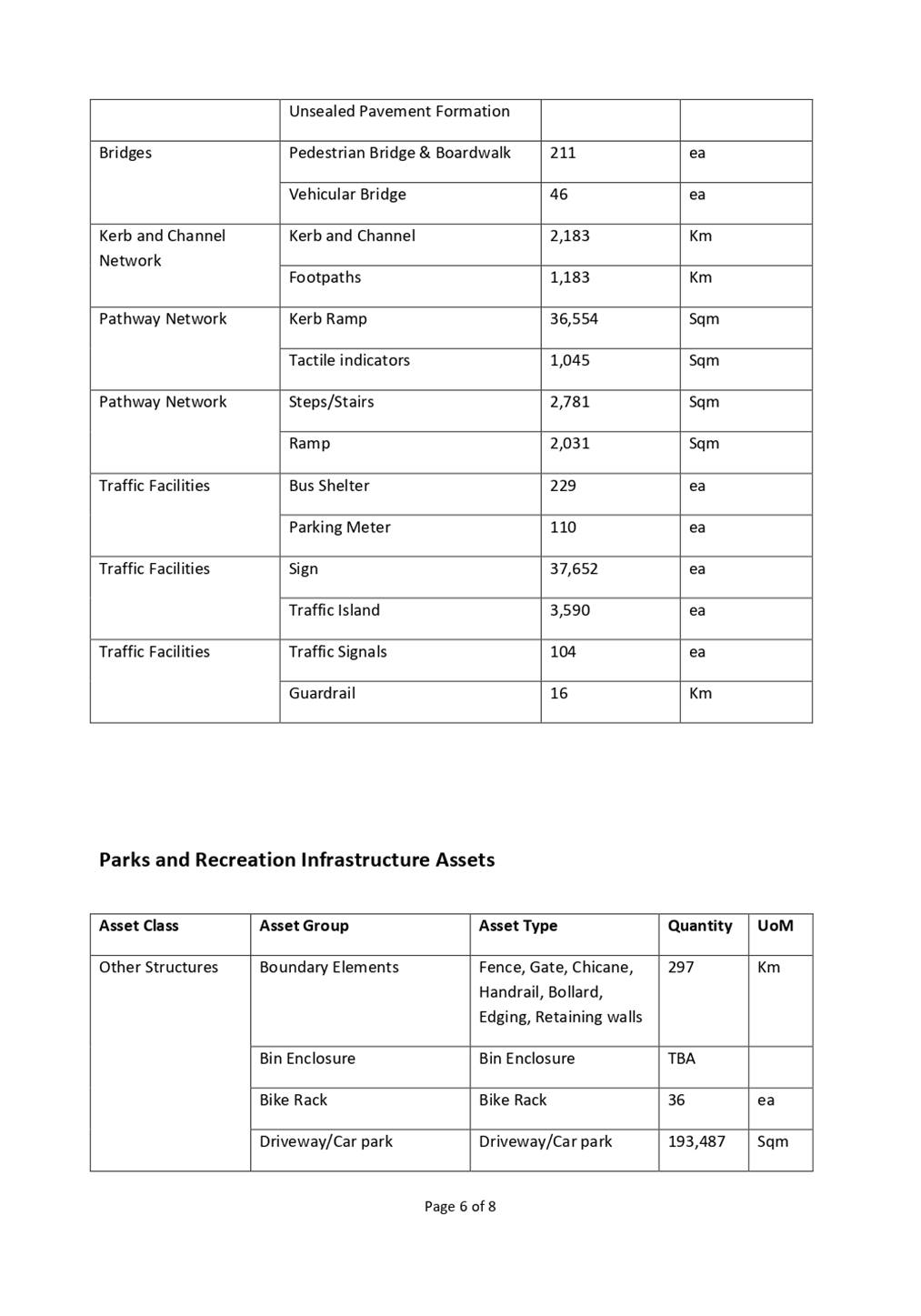

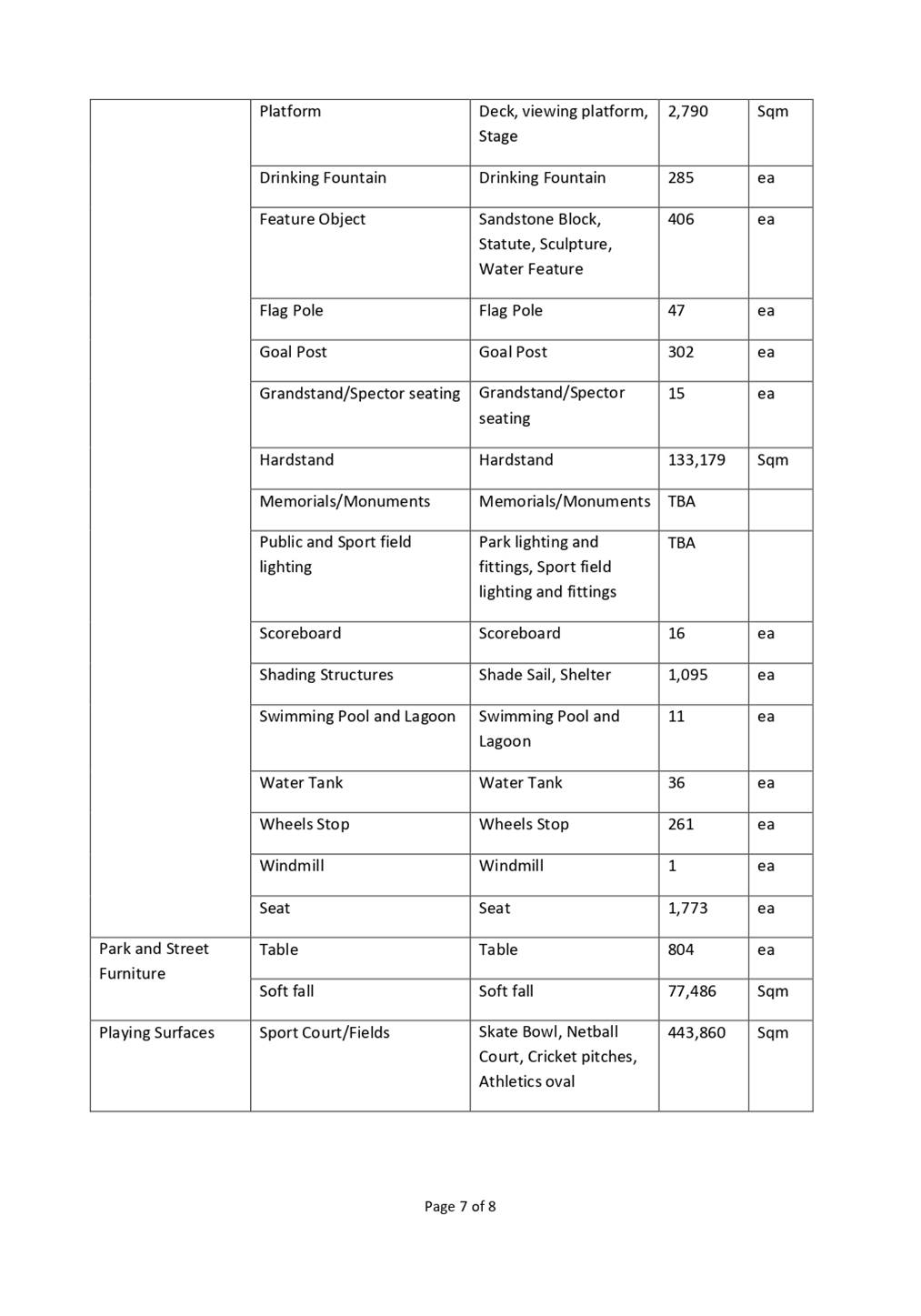

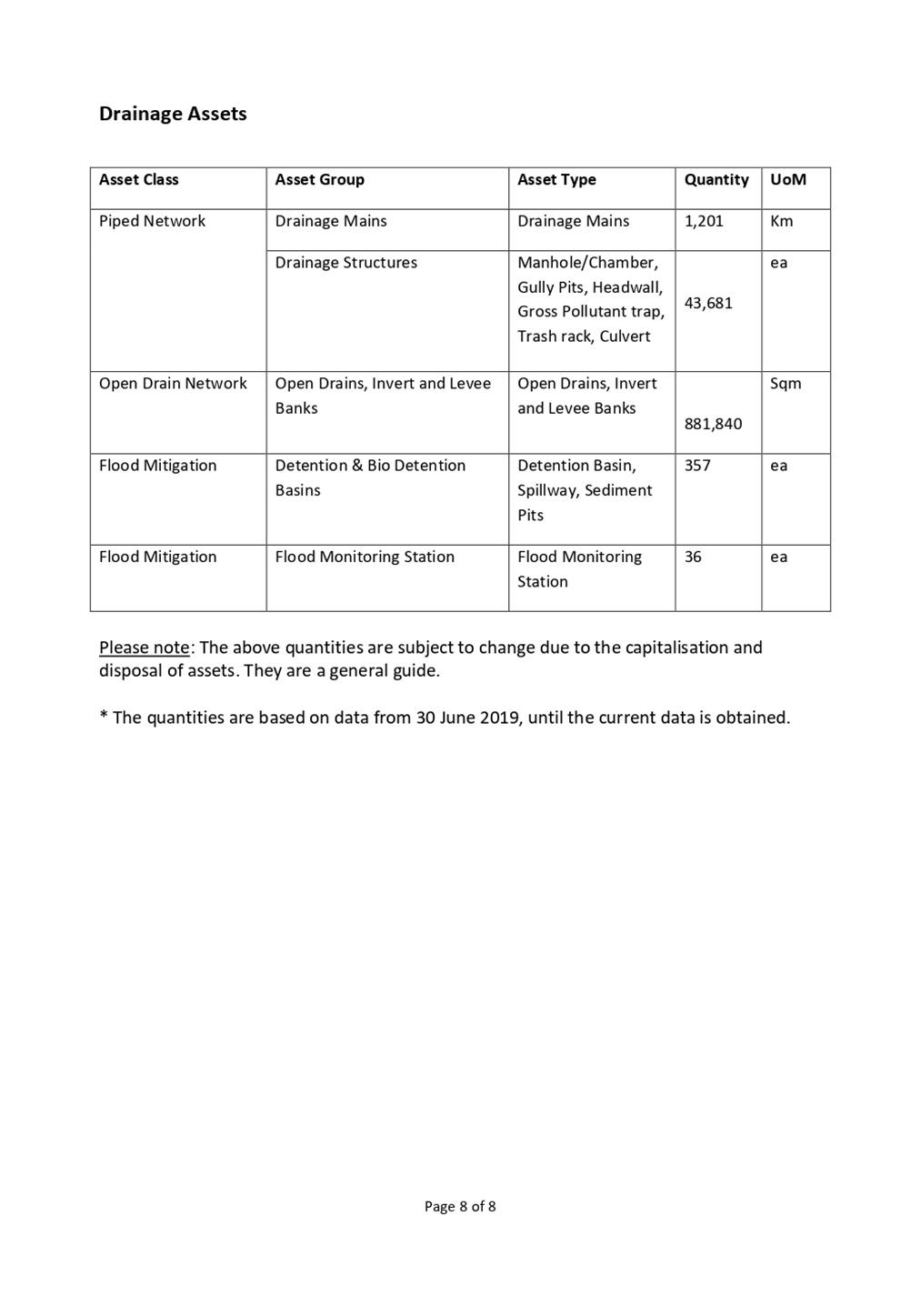

The report outlines the asset classes to be revalued over the next five years and attachment 1 details the project specification for asset valuation services of Council’s assets.

Attachments and Confidential Background Papers

|

1. |

2020 Project Specification - Land Buildings and Structures

and Infrastructure Assets ⇩ |

Barbara Watson

Principal Financial Accountant

I concur with the recommendations contained in this report.

Jeffrey Keech

Finance Manager

I concur with the recommendations contained in this report.

Andrew Knight

General Manager - Corporate Services

“Together, we proudly enhance the quality of life for our community”